Why Asset Location Matters in Financial Planning: How Taxes Impact Portfolio Outcomes

by Phil Tull | June 15, 2026 | Investment Planning, Tax Planning

LOCATION. LOCATION. LOCATION.

You’ve heard it before—and for good reason. In real estate, this phrase has guided decisions for over a century because it captures a simple truth: where something is matters just as much as what it is.

Why Location Still Reigns Supreme

Location shapes values in three powerful ways:

- Location affects access to jobs, schools, transportation, and lifestyle amenities.

- Land location is fixed—you can renovate a home, but you cannot move it.

- Desirable locations tend to retain value and liquidity over time.

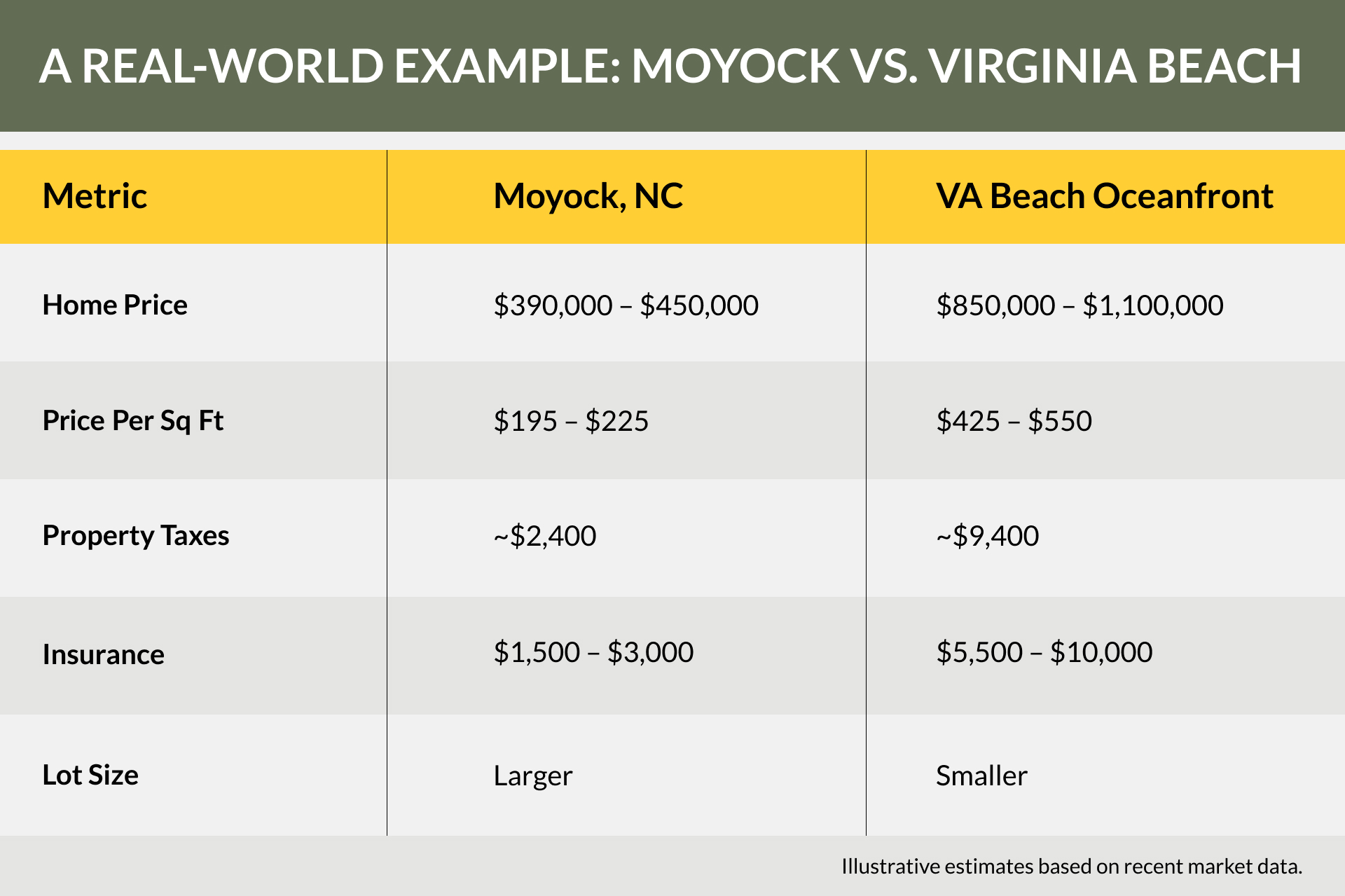

A Real-World Example: Moyock vs. Virginia Beach

Let’s bring this closer to home with a Mid-Atlantic comparison: a 3‑bedroom, 2‑bath, ~2,000-square-foot single-family home in Moyock, NC (Currituck County) versus Virginia Beach, VA (Oceanfront).

It’s not just the sticker price.

When you factor in property taxes and insurance, owning near the Virginia Beach oceanfront could cost an additional $11,000-$14,000 per year—that’s roughly $900-$1,150 per month. Yes, lifestyle, commute, and community matter. But purely from a cost perspective, location has a lasting impact on your cash flow and long-term wealth.

Location Matters in Investing, Too

Here’s the twist: location isn’t just about real estate but is just as important in financial planning.

One million dollars in a Traditional IRA is not the same as $1 million in a Roth or taxable brokerage account. Why? One word… TAXES.

Where your assets are held can make a significant difference in your overall portfolio value over time, which is why tax-efficient asset location is an important part of long-term financial planning. Because at the end of the day, it’s not what you earn, but what you keep after taxes. This is also where guidance from a financial advisor can help you understand how taxes, account types, and long-term goals work together.

How Financial Advisors Use Asset Location in Financial Planning

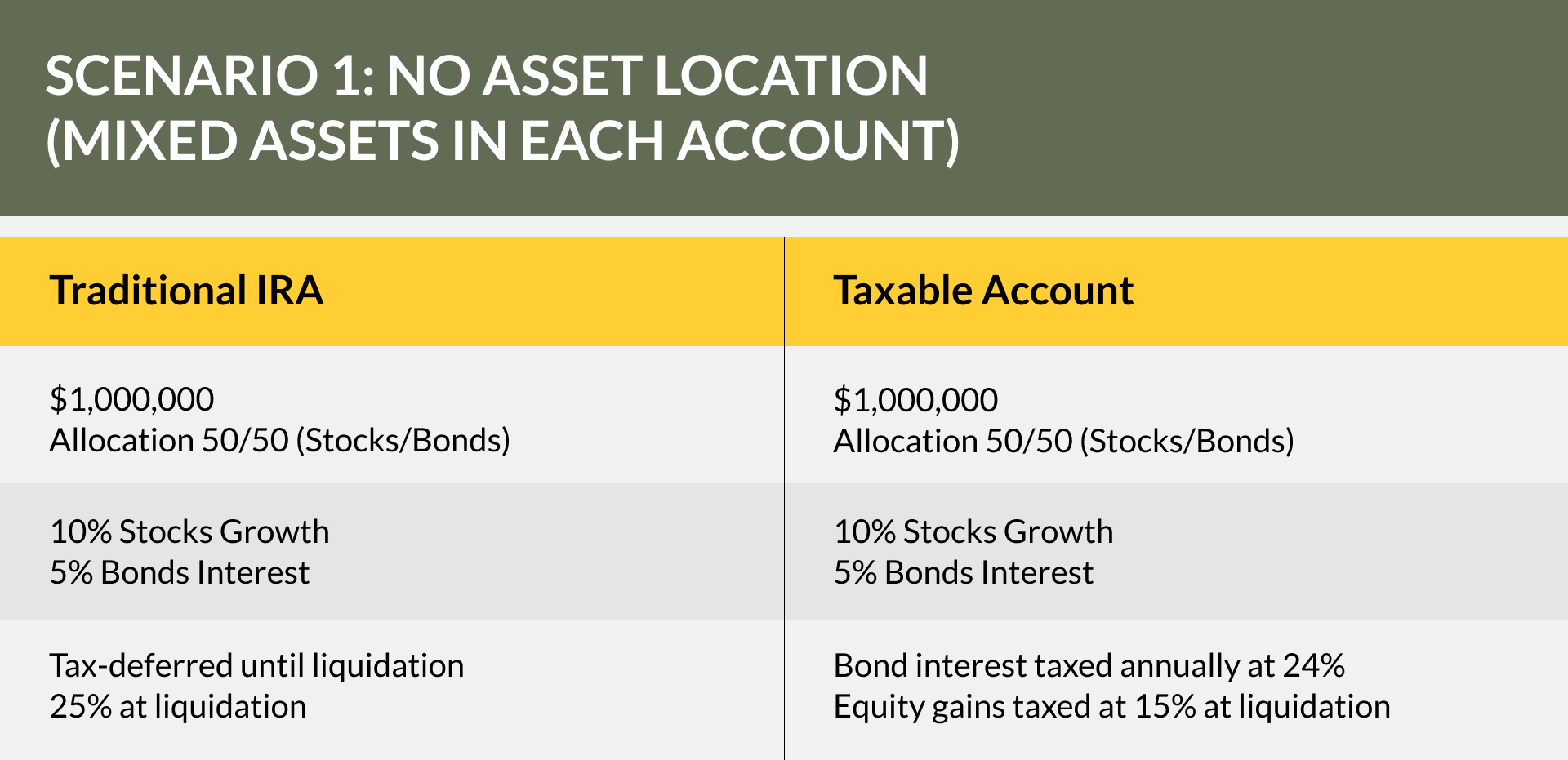

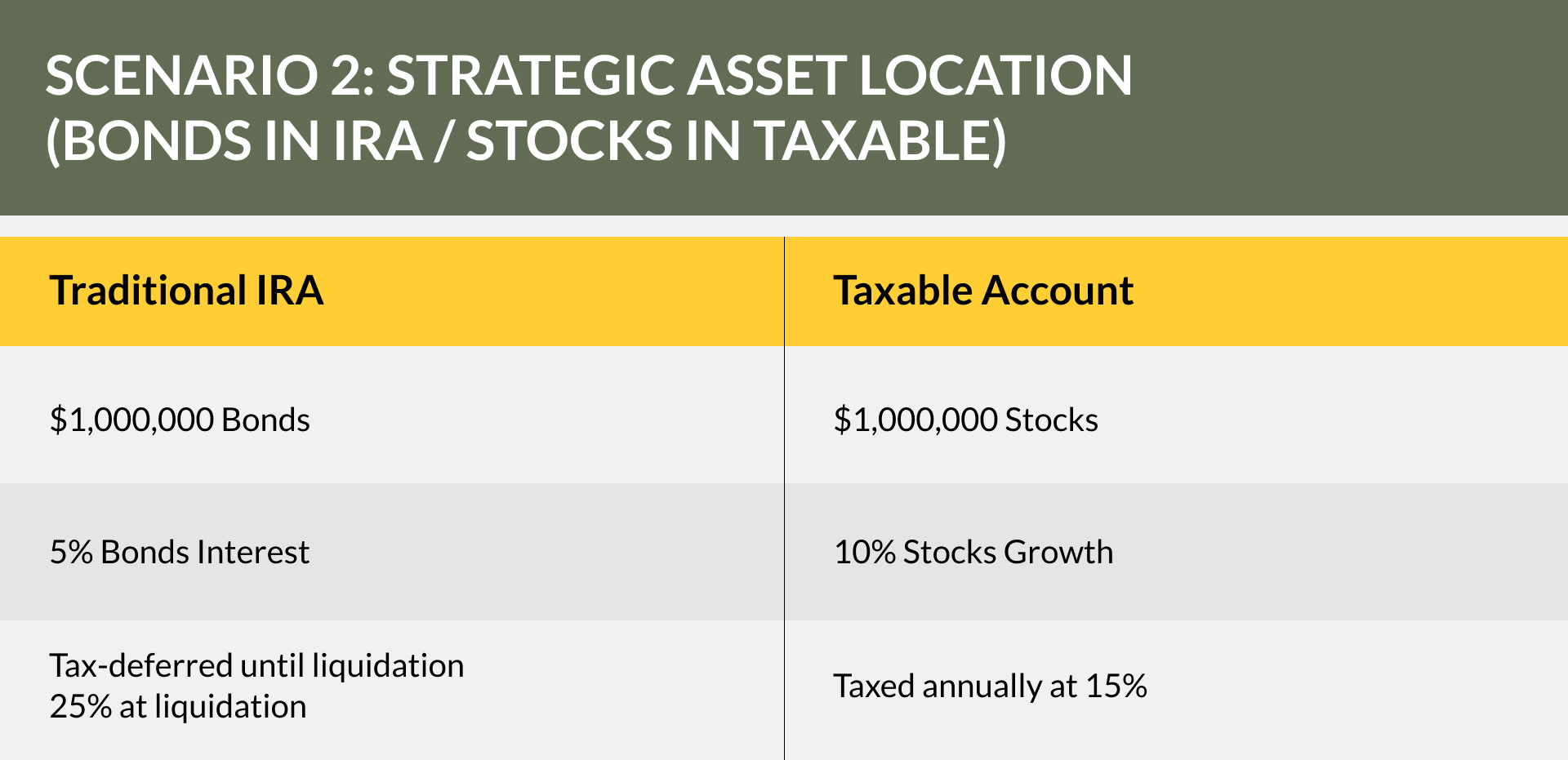

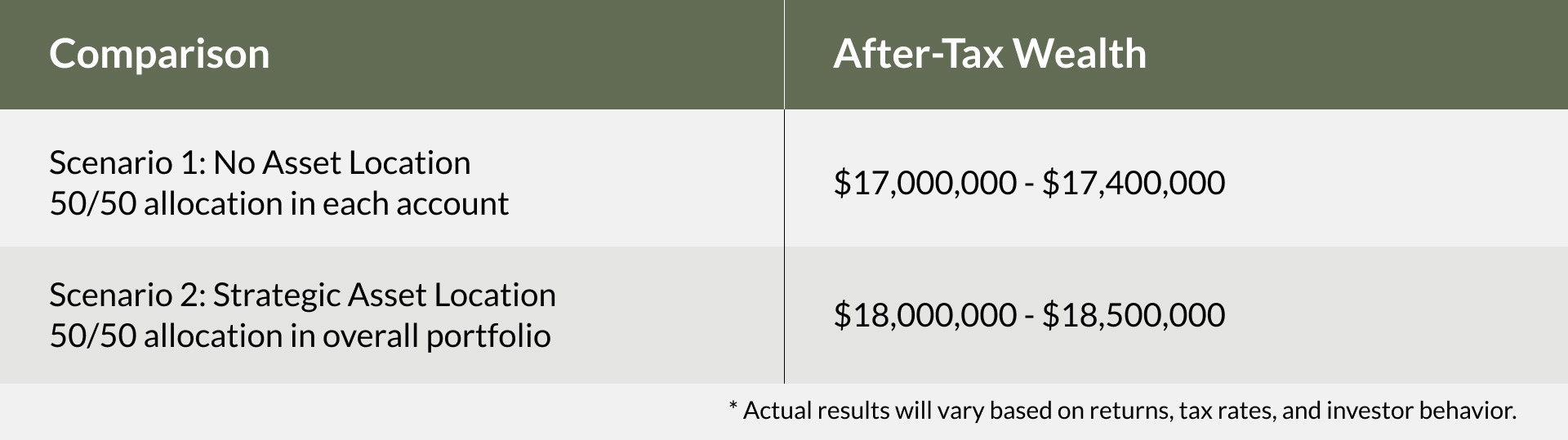

Let’s simplify how financial advisors evaluate asset location by comparing the after-tax growth of two portfolio structures over time.

Starting Point: An investor has:

- $1,000,000 in a Traditional IRA

- $1,000,000 in a taxable brokerage account

- $2,000,000 total portfolio value

- Target allocation of 50% stocks and 50% bonds

This approach uses strategic asset placement to align investments with the accounts where they may receive more favorable tax treatment.

Impact Over 30 Years:

- Equity growth is ultimately taxed as ordinary income.

- Bond interest suffers ongoing annual tax drag.

- Lower after-tax ending value.

Under these assumptions, asset location produces approximately $1 million more in after‑tax wealth without increasing portfolio risk.

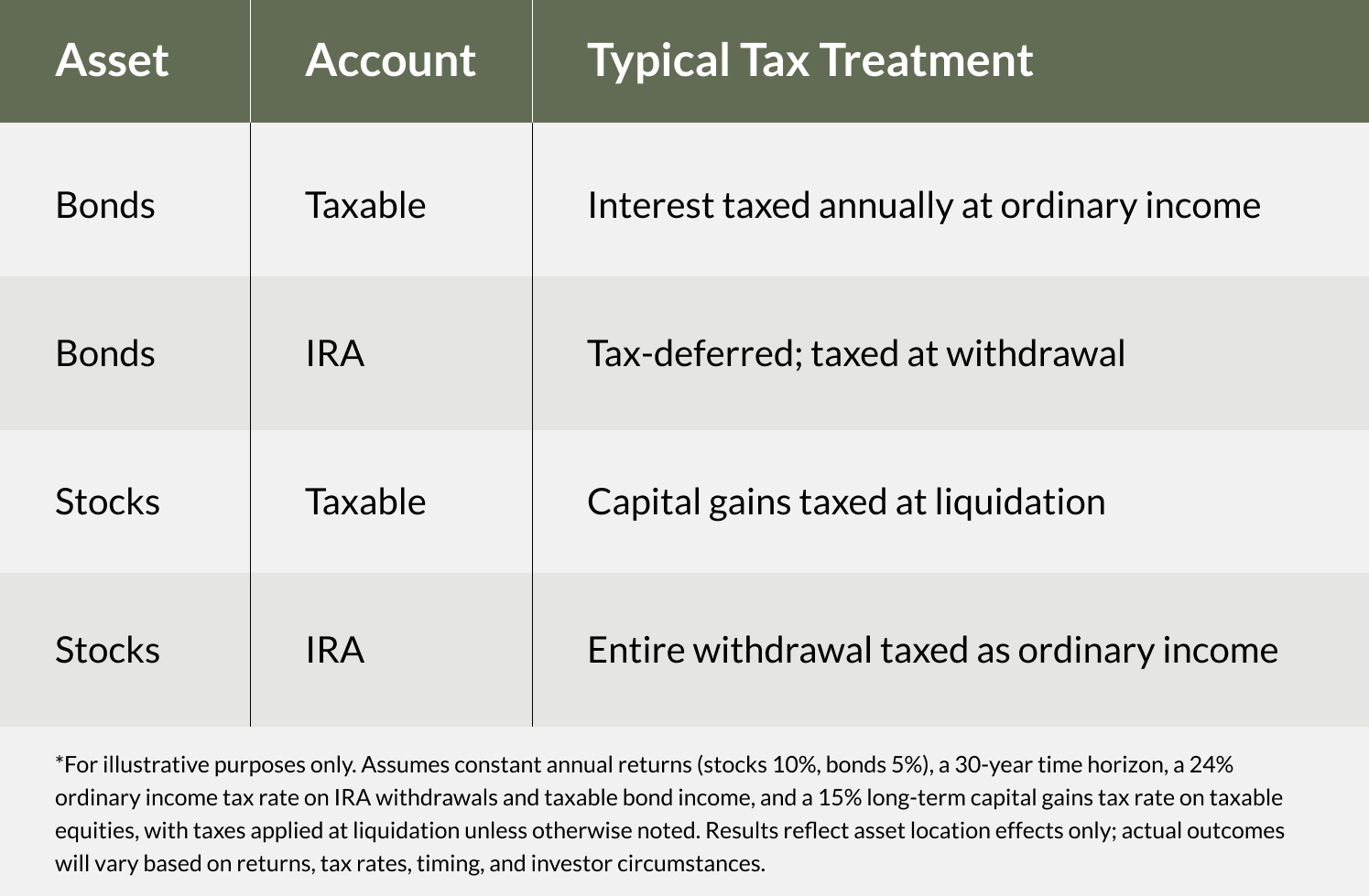

How to Think About Asset Location

Here is a simple priority list to consider when evaluating your portfolio for asset location opportunities and practically applying tax-smart portfolio planning.

Priority 1: Least Tax‑Efficient Assets (Best suited for tax-deferred accounts)

- Taxable bonds

- High‑yield bonds

- REITs

- Actively managed funds

Priority 2: Moderately Tax‑Efficient Assets (Consider Roth)

- Dividend‑heavy equities

- Balanced / allocation funds

- Factor strategies with higher turnover

Priority 3: Most Tax‑Efficient Assets (Roth or Taxable Brokerage Accounts)

- Broad‑market equity index funds

- Total market exchange-traded funds (ETFs)

- Buy‑and‑hold growth equities

Let’s Make Your Location Work For You

Just like buying the wrong home location can cost you thousands each year, placing investments in the wrong accounts can cost you hundreds of thousands—or more—over time. The difference is subtle and often overlooked.

Optimizing your investment “location” requires thoughtful planning across tax strategy, retirement income and long-term goals. That’s where a fee-only investment advisor acting as a fiduciary like Tull Financial Group comes in.

At Tull Financial Group, we work with clients to bring clarity and structure to these decisions, helping to ensure each piece of the plan is aligned and working efficiently. One of our experienced advisors would be happy to explore how these strategies could apply to your financial situation. Contact us today to schedule a complimentary consultation at (757) 436-1122.