Your retirement savings may be getting a tax hit!

If you’re age 50 or older, you may already know about catch-up contributions, the extra amount you can contribute to your retirement plan beyond the standard annual limit. However, recent changes under the SECURE 2.0 Act have raised an important question: Do income limits affect your ability to make these contributions?

The short answer: No, income does not disqualify you from making catch-up contributions. However, your income may determine how those contributions are treated for tax purposes.

What Changed Under SECURE 2.0?

Starting in 2026, if you earned more than $150,000 in wages (adjusted for inflation) from your employer in the previous year, any catch-up contributions you make to a 401(k), 403(b), or governmental 457(b) plan must be made as Roth contributions.

Here’s what that means for you:

- If your wages were $150,000 or less:

You can choose pre-tax or Roth for your catch-up contributions. - If your wages were more than $150,000:

You can still make catch-up contributions, but they must be Roth (after-tax).

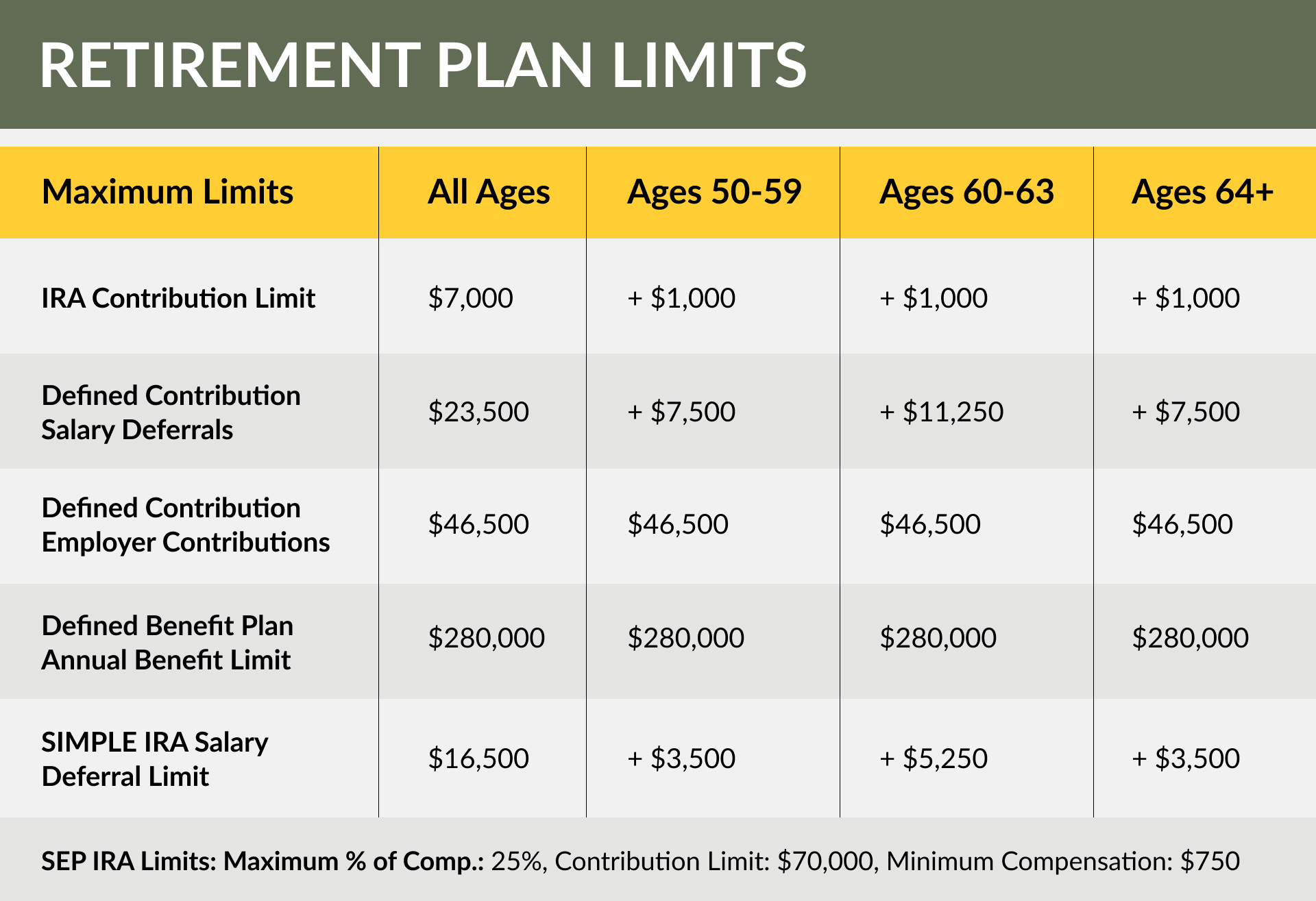

2025 Contribution Limits At-A-Glance

Plans Exempt From the Rule:

- SIMPLE IRAs, SEP IRAs, SARSEPs, Starter 401(k) plans, and certain governmental and collectively bargained plans (which may have delayed applicability).

Read Also: Financial Planning Insight on Roth IRA Conversions

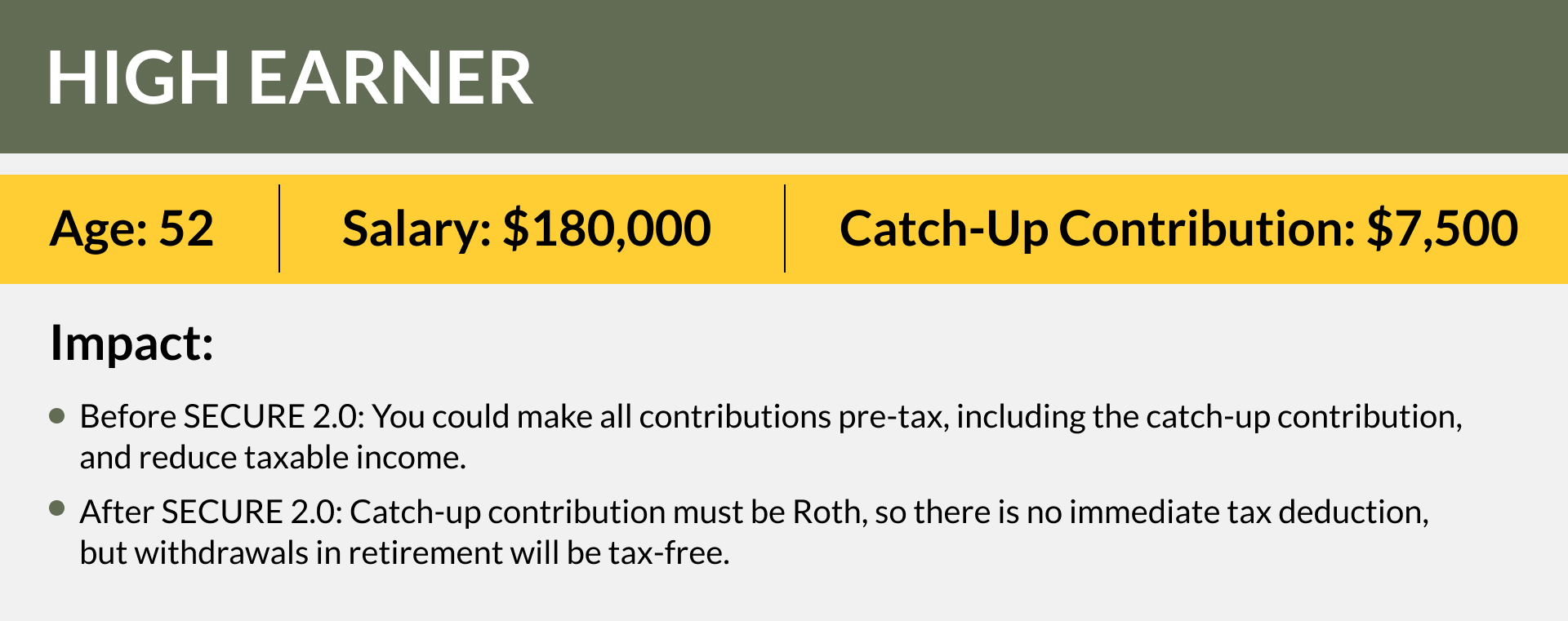

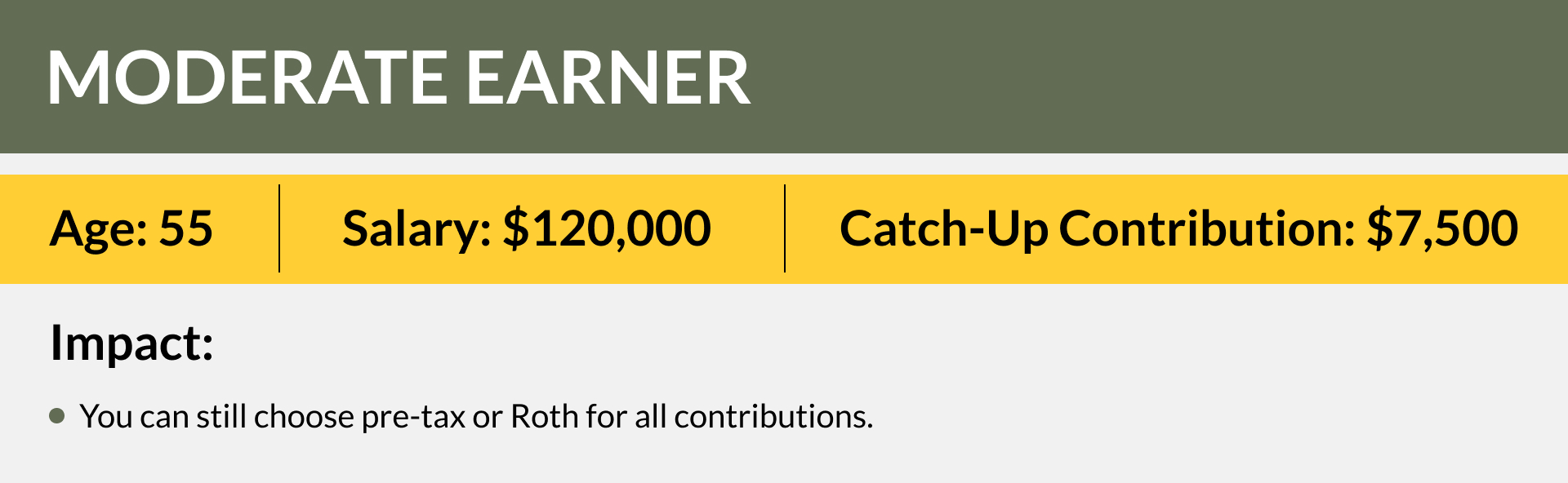

Examples of the Roth Catch-Up Impact

Why This Matters

This change could impact your tax planning strategy. Roth contributions mean you pay taxes now, but withdrawals in retirement are tax-free. If you’re in a high-income bracket today and expect a lower bracket in retirement, this shift could affect your overall retirement plan.

Next Steps

- Check your income level from the prior year to see if the Roth rule applies.

- Review your retirement plan options—does your employer offer Roth contributions?

- Talk to your financial advisor about how this change fits into your long-term tax strategy.

Need Help Navigating these Changes?

At Tull Financial Group, we specialize in helping clients make informed decisions about retirement planning. Contact us today to discuss your strategy.

The SECURE Act 2.0 Effective Dates Explained

The SECURE Act 2.0 was signed into law on December 29, 2022, as part of the Consolidated Appropriations Act, 2023. Its provisions have staggered effective dates, meaning different parts of the law took effect at different times due to two main reasons. First, implementing the changes at scale by custodians and plan sponsors could not be done overnight and would take time. Second, some of the changes were found lacking in specifics and required further clarity before taking effect.

Here are some of the retirement specific key effective dates:

Effective Immediately (December 29, 2022)

- Some Roth contribution options for employers.

- Certain changes to required minimum distributions (RMDs).

Effective January 1, 2023

- RMD age increased from 72 to 73.

- Reduced penalty for failing to take RMDs.

- New rules for Qualified Charitable Distributions (QCDs).

Effective January 1, 2024

- Inflation indexing for QCD limits.

- Some provisions related to SIMPLE and SEP Roth IRAs.

Effective January 1, 2025

- Automatic enrollment required for new 401(k) and 403(b) plans.

- Higher catch-up contribution limits for individuals aged 60–63.

Effective January 1, 2026

- Catch-up contributions for high-income earners must be made as Roth contributions (the “Rothification” rule)